Paycheck Protection Program Loan Forgiveness: Make Sure to Know the Provisions

Prepared by David B. Walston

April 13, 2020

As most employers know, a key feature of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) is its Paycheck Protection Program (PPP) that allows employers to obtain loans that may be “forgiven” if used for specified costs. The amount of PPP forgiveness is tied to additional requirements. Unfortunately, the application of several key forgiveness provisions is less than clear and the federal regulatory agencies charged with the administration of the PPP have not published sufficient guidance to assist employers. This article summarizes the key forgiveness provisions and identifies the questions that have not been answered to date.

Forgivable Use of Loan

- Payroll Costs

- Cost of employee benefits:

- Health, dental, vision, STD/LTD, life insurance premiums

- Cafeteria plan

- Retirement benefits

- Paid time-off (Does not include payments under the Emergency Paid Sick Leave Act and Emergency Medical Leave Expansion Act – these expenses are recouped through tax credits)

- State and local income taxes paid by the employer (Does not include payroll taxes paid by the employer)

- Severance benefits

- State and local income taxes paid by the employer (Does not include payroll taxes paid by the employer)

- Cost of employee benefits:

- Mortgage interest (not principal payments or pre-payment fees)

- Rent

- Utilities

- Interest ton debt obligations (obligation incurred before 2.15.20)

THE EMPLOYER MUST USE 75% OF LOAN TOWARD “PAYROLL COSTS.”

Reductions in Forgiveness

Apart from using loan proceeds properly, there are two hurdles to 100% forgiveness of the loan – Employee Retention and Compensation Retention.

Although there is no clear guidance from federal regulatory agencies, the general assumption is that the reductions from failing to meet Employee Retention ad Compensation Retention requirements are applied against the amount the employer uses to cover payroll costs.

Example:

Total PPA loan of $500,000

At least $375,000 (75%) must be used toward Payroll Costs.

The other $125,000 (25%) may be used for any combination of the other qualifying costs

If this is an interpretation that will be applied, assuming a 10% Employee Retention “penalty” against loan forgiveness, the reduction would be applied against the $375,000 as opposed to the full $500,000 amount of the loan.

- Employee Retention

The amount of loan forgiveness may be reduced based on the percentage reduction of the number of “full-time equivalent employees” the employer has at times specified in the Act.

-

- Counting Employees

1. The average of full-time equivalent employees for each month is derived from averaging the number of full-time equivalent employees for each pay period during a month.

2. Employees on payroll, not whether the employee worked during the payroll period

3. “Full-time equivalent employee:” The CARES Act of 2020 does not define “full-time equivalent employee” but the concept is used in the Affordable Care Act). It is logical to expect that the Affordable Care Act definition will transfer to the CARES Act.

Full-time employees – All employees working 30 hours or more per workweek on a regular basis

÷

The number reached by dividing all hours worked by part-time employees during a month by 120

Example:

40 employees regularly working more than 30 hours per workweek

20 part-time employees work a combined 1,600 hours in a month.

[40 + (1,600 ÷ 120)] = 53 FTE

B. Reduction by Headcount Loss

Mathematical equation

The employer is allowed to select from two options

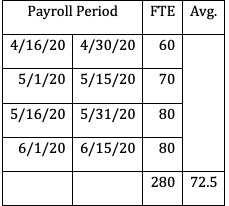

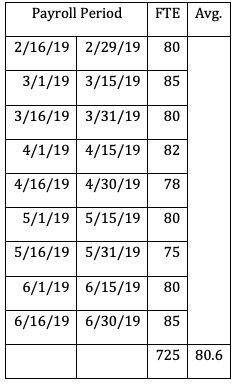

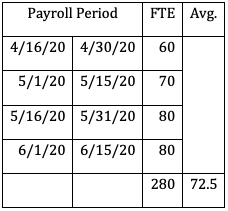

OPTION 1: Assumes loan proceeds received on 4.14.20

The average number of FTE’s per month for the 8 week period from the date the loan proceeds are available

÷

The average number of FTE’s per month between 2.15.19 and 6.30.19

80.6 ÷ 72.5 = 90% Employee Retention.

Loan Forgiveness reduced by 10%

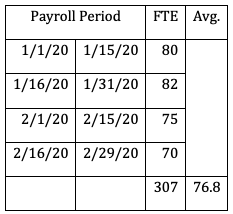

OPTION 2: Assumes loan proceeds on 4.14.20

The average number of FTE’s per month for the 8-week period from the date the loan proceeds are available

The average number of FTE’s per month for the 8-week period from the date the loan proceeds are available

÷

The average number of FTE’s per month between 1.1.20 and 2.29.20

76.8 ÷ 72.5 = 94% Employee Retention

6% reduction in loan forgiveness

C. Safe Harbor

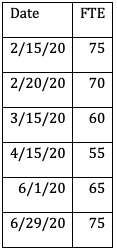

If an employer separates employees between February 15, 2020, and April 26, 2020, there will be no reduction in loan forgiveness IF by June 30, 2020, the employer recalls, un-furloughs, re-hires or hires a sufficient number of employees to return to the number it had on 2/15/20.

Example: Employee count set as of 2/15/20

Five FTE lay-off on 2/20/20

Ten FTE lay-off on 3/15/20

Five FTE lay-off on 4/15/20

Ten FTE re-hire on 6/1/20

Ten FTE re-hire 6/29/20

No reduction in loan forgiveness.

2. Compensation Retention

As a separate reduction, loan forgiveness can be reduced due to reductions in the compensation of an employee.

-

- General

The reduction is based on a comparison of the compensation paid to an employee making less than $100,000 on an annualized basis.

$3,846.15 gross for a bi-weekly payroll = $100,000 annualized

$4,166.66 for a semi-monthly payroll = $100,000 annualized

For the employees falling under the $100,000 exclusion, the reduction is based on an examination of each individual employee’s compensation.

The CARES Act provides:

The amount of loan forgiveness … shall be reduced by the amount of any reduction in total salary or wages of any employee … during the covered period that is in excess of 25% the total salary or wages of the employee during the most recent full quarter during which the employee was employed before the covered period.

Read literally, the equation is:

Total compensation received by the employee in the

8 week period after loan proceeds are available for use

Total compensation received by the employee between

1.1.20 and 3.31.20

The strict application of this formula looks as follows;

Example 1: Employee employed the entire period 1.1.20 – 3.31.20 and makes $1,250 per week.

Employee’s weekly compensation is reduced 1% from $1,250 to $1,237.50.

Employee is paid a total of $9,900 during the 8-week period $1,237.50.

Employee was paid total $15,000 ($1,250 x 12 wks) from 1.1.20 – 3.31.20

$9,900 ÷ $15,000 = .66

Employer would lose 9% of forgiveness for the 1% pay reduction

.75 – .66 = .09

$9,900 x .09 = $891 not forgiven for that employee

This calculation would have to be run for every employee.

Such a result would be absurd. However, to date, there are no regulations that instruct employers how the Compensation Retention provision will be interpreted. This may soon change, but at present employers are left with no clear guidance.

B. Safe Harbor

The Compensation Retention provision has a clear safe harbor:

If an employer reduces the compensation of an employee between February 15, 2020, and April 26, 2020, there will be no reduction in loan forgiveness IF by June 30, 2020, the employee’s compensation returns to its previous level.

Until guidance is issued, the Compensation Retention safe harbor is the only option through an employer knows without a doubt there will be no reduction based on reducing employees’ compensation.

The CARES Act of 2020 and the Families First Coronavirus Response Act have thrown a great amount of statutory and regulatory interpretation at employers. The Department of Labor has stepped forward with its temporary regulations and Questions and Answers for the Families First Coronavirus Response Act. The Treasury Department has issued several publications of its own, but none address the ambiguities identified above. When the Treasury Department does issue guidance, we will provide you additional information regarding the avenues available to employers to ensure maximum forgiveness of am PPA loan.

If you need assistance navigating the Paycheck Protection Program, please contact:

David B. Walston

dbwalston@csattorneys.com

205.250.6636

About Christian & Small

Christian & Small LLP represents a diverse clientele throughout Alabama, the Southeast, and the nation with clients ranging from individuals and closely-held businesses to Fortune 500 corporations. By matching highly experienced lawyers with specific client needs, Christian & Small develops innovative, effective, and efficient solutions for clients. With offices in Birmingham, metro-Jackson, Mississippi, and the Alabama Gulf Coast, Christian & Small focuses on the areas of litigation and business, is a member of the International Society of Primerus Law Firms, and is the only Alabama-based member firm in the Leadership Council on Legal Diversity. Our corporate social responsibility program is focused on education, and diversity is one of Christian & Small’s core values.

No representation is made that the quality of legal services to be performed is greater than the quality of legal services performed by other lawyers.